Your hospital bill is not final. Here is how millennials are cutting theirs by 40-80%.

The number on that statement is a starting point, not a final answer and most patients have no idea they can push back.

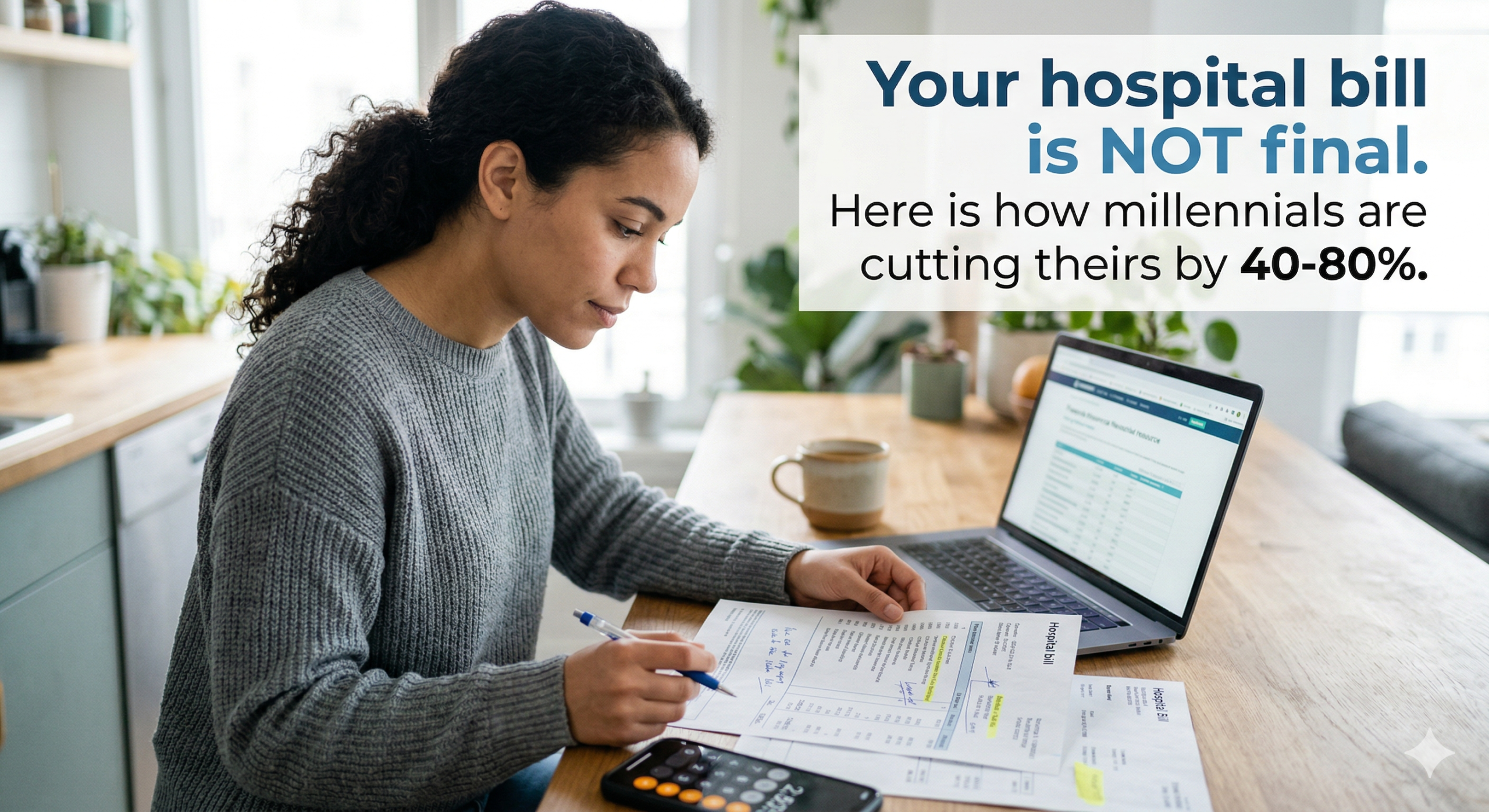

You opened it. The bill sitting on your kitchen counter with a number that made your stomach drop. Maybe it is $4,000. Maybe it is $40,000. Either way, your first instinct was probably to pay it fast, hide it from your partner, or just not think about it at all.

All three of those instincts will cost you money. Here is what actually works.

80% of hospital bills contain at least one billing error

$1,300 average billing overcharge per patient (2023)

57% of US hospitals are nonprofits required to offer free care

The chargemaster rate is not what you actually owe

Every hospital has something called a chargemaster — an internal price list where every service has a sticker price set as high as possible. Insurance companies negotiate it down. Medicare pays a fraction of it. You, as a cash or underinsured patient, are being handed the sticker price and told it is due upon receipt.

It is not. The chargemaster rate is a ceiling, not a floor. Your job is to find out where the floor actually is.

“The amazing thing here is a medical service provider submitted a bill that was 80 percent higher than what they would accept. This kind of price gouging is illegal in many businesses.”— r/personalfinance

Do not pay before doing this one thing

The single most valuable move you can make before touching your wallet is requesting a fully itemized bill. Not the summary you received in the mail. A line-by-line breakdown of every charge, with the five-digit CPT code for each service.

SCRIPT — SAY THIS ON YOUR FIRST CALL

“Hi, my name is [name] and my account number is [number]. Before I make any payment, I need a fully itemized bill showing every individual charge, the CPT code for each charge, and the date of service for each item. Can you send that by email as a PDF? What is the turnaround time?”

Then look up every CPT code on the CMS Medicare fee schedule at cms.gov. That number — what Medicare pays for the same service — is your negotiating baseline. Hospitals routinely charge 3 to 10 times that rate.

The 3 calls that cut most bills in half

- 1 Call 1: Request the itemized bill and ask for a hold on collections while you review. Ask if they have a financial assistance or charity care program — and request an application on the same call.

- 2 Call 2: Go through your dispute list, charge by charge. Flag duplicates, upcoded procedures, services you never received. Then apply for financial assistance before doing anything else. Most patients skip this entirely — it can wipe out the bill completely.

- 3 Call 3: Once errors are corrected and assistance is decided, negotiate a lump-sum settlement. Open at 40-50% of the corrected balance. Stay quiet after your offer. Let them respond.

If you have insurance, check your Explanation of Benefits (EOB) before Call 2. If the hospital is billing you more than what your EOB says you owe, that is not a negotiation — it is a billing error. You are owed a correction.

The program most patients never apply for

Every nonprofit hospital in the United States is required by federal law to maintain a charity care program — free or heavily discounted care for patients who cannot afford to pay. In 2025, 400% of the Federal Poverty Level is approximately $124,000 for a family of four. You may qualify even if you feel like you have a decent income.

Apply before making any payment. Some hospitals reject applications from patients who have already started paying because partial payment signals you can cover the full balance.

“I used the 3-call system in this guide on a $34,000 hospital bill. Settled for $11,200. That’s $22,800 back in my pocket.”— r/personalfinance community member

What happens if it goes to collections

Here is something most people do not know: a CFPB rule finalized in 2025 removed medical debt under $500 from credit reports entirely, and restricted how larger balances can be reported. The power collectors have over your credit score is significantly smaller than it used to be.

If debt has already gone to a collections agency, send a debt validation letter via certified mail before paying a cent. This forces the agency to prove the debt is valid and they have the right to collect it. Until they verify it in writing, all collection activity must stop — calls, letters, credit bureau reporting. Every violation is worth up to $1,000 in statutory damages.

The one rule before you pay any settlement

Whatever number you agree to, get it in writing before your money moves. The letter must confirm the exact settlement amount, that it satisfies the balance in full, and that the account will not be referred to further collections. Verbal agreements are not enforceable. Pay by check or money order only — never by card over the phone.

“$1,600 bill negotiated down 20 percent, and then finally down to the original $300 quote. Just a reminder that they aren’t set in stone and all it takes is a phone call.”— r/personalfinance

Most people who follow this full process error audit, financial assistance, lump-sum negotiation end up paying 20 to 50% of the original billed amount. The work takes 2 to 4 weeks and 3 phone calls. The alternative is paying full chargemaster rate on a number that was never meant to be paid.

Want the full playbook for FREE?

The Hospital Bill Fight Kit walks you through the complete process — 9 word-for-word scripts, the full debt validation letter, hardship statement template, and a quick-reference script index. Everything you need from bill to zero balance.

Leave an honest review to get it completely FREE. Limited to the first 100 people.